Credit cards are one of the fastest, most convenient ways for businesses to get paid. They speed up cash flow, simplify collections, and give customers flexibility. According to the Federal Reserve’s 2025 Diary of Consumer Payment Choice, credit cards accounted for 35% of all consumer payments in 2024, up 18% in 8 years. For businesses, that trend makes accepting credit cards less of a convenience and more of a necessity to keep up with how customers prefer to pay.

The tradeoff is that accepting them comes with a cost. On a $10,000 invoice, processing fees typically run anywhere from 2% to 3%, and across a full year of transactions, those numbers add up.

For most small and mid-market companies, processing fees have always been treated as a fixed cost of doing business. However, there’s good news. A growing number of businesses are finding ways to offset that expense without changing how they accept payments. They’re turning to a practice called surcharging, and it’s giving them a way to protect their margins while still offering customers their preferred payment option.

What Surcharging Actually Means (and What It Doesn’t)

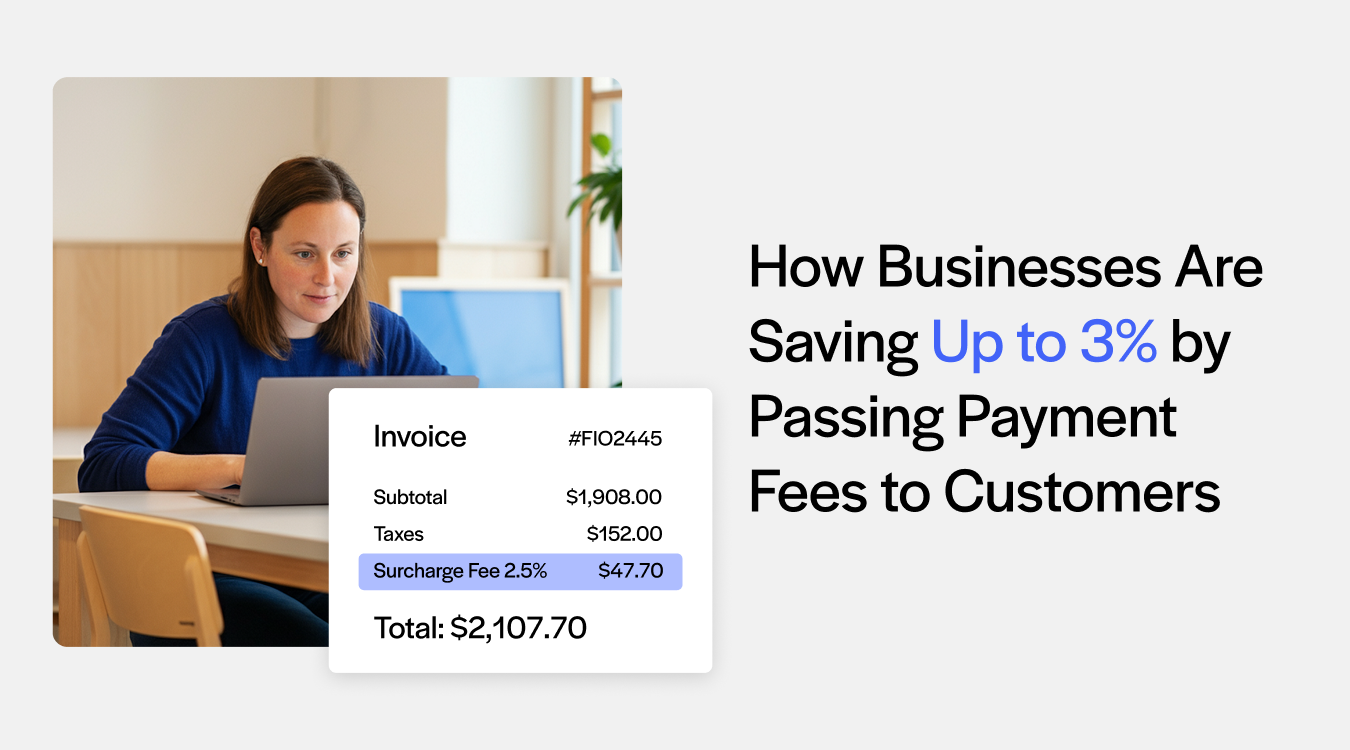

At its core, surcharging is straightforward. When a customer pays with a credit card, the merchant adds a small fee to the transaction to cover the cost of processing that payment.

It’s worth pausing here because surcharging gets confused with other things.

• It’s not a convenience fee, which is a flat charge for using a non-standard payment channel.

• It’s not a price hike disguised as a processing cost, nor is it a penalty for choosing plastic over cash.

Think about it this way. When a customer writes you a check, you don’t pay a card network 3% for the privilege of depositing it. When they send an ACH payment, the cost to process it is a fraction of what a credit card costs. Surcharging is the business being more transparent about the fees they take on to run their business. Customer sees what credit card processing actually costs, and they can either pay it or choose a payment method that doesn’t carry a fee.

Why So Many Businesses Are Making the Switch Now

There’s a reason surcharging has picked up so much traction recently. It’s not just one factor. It’s a combination of pressures that have been building over the past few years.

1. For starters, processing fees have gone up. The average interchange rate has crept higher.For businesses processing six or seven figures in credit card payments annually, even a small percentage increase translates into real money. A wholesale distributor processing $500,000 a month in card payments could be spending $150,000 or more per year just on fees.

2. Credit card usage is still climbing. Cards now account for roughly a third of all consumer payments in the United States. In B2B transactions, they’re becoming increasingly common for everything from recurring invoices to large purchase orders. The more your customers pay by card, the more you end up paying in fees.

3. Customers have gotten used to seeing surcharges. They show up at gas stations, medical offices, and government agencies. According to recent surveys, over half of credit card holders have encountered a surcharge at some point. It’s no longer unusual.

The Legal Side: Where Surcharging Stands Today

One of the biggest misconceptions about surcharging is that it’s legally risky. Surcharging is legal in the vast majority of U.S. states, but a handful still restrict or prohibit it.

As of early 2026, states like Connecticut, Massachusetts, Maine, and California have laws that either ban surcharging outright or impose limitations. Some states allow it with specific rules. Colorado caps surcharges at 2% of the transaction. New York requires that merchants can only pass along their actual cost of acceptance, and the disclosure requirements are strict.

On the federal level, there’s no law prohibiting surcharges. Visa caps them at 3% of the transaction, while Mastercard allows up to 4%. Both networks require that the surcharge never exceeds the merchant’s actual cost of processing.

One detail to note: you can only surcharge credit card transactions. Debit cards and prepaid cards are off-limits under the Durbin Amendment. That’s not a gray area. That’s federal law.

If you’re a CFO or billing manager thinking about surcharging, the legal landscape shouldn’t scare you off. It just means you need to do your homework.

• Know the rules in every state where you do business

• Make sure your surcharge doesn’t exceed the caps

• Be transparent with your customers.

Getting It Right: Communication Is Everything

There’s a right way and a wrong way to roll out surcharging. The difference usually comes down to how well you communicate it.

Your customers need to know about the surcharge before they complete their transaction, not after. In a brick-and-mortar setting, that means signage at the entrance and at the point of sale. For online payments, it means showing the fee clearly on the checkout page, broken out as a separate line item, before the customer clicks “Pay.”

On invoices, a short note is usually all it takes. Something like: “A 3% processing fee applies to credit card payments. No fee for ACH or check.” Clear, direct, and hard to miss.

The language matters, too. Don’t call it a “convenience fee” if it’s a surcharge, and don’t bury it in fine print. Be upfront, be clear, and be consistent.

Why Automation Matters More Than You Think

Manually calculating surcharges on every transaction is not only tedious, but also a compliance risk. If your system accidentally applies a surcharge to a debit card transaction, or charges more than your actual processing cost, you could face penalties from the card networks or the state law.

For any business processing more than a handful of card payments, automation isn’t optional. It’s essential. The right payment platform should apply surcharges only to eligible credit card transactions, automatically exclude debit and prepaid cards, calculate the correct percentage, and display the fee clearly on receipts and invoices.

This is where embedded payments come in. Modern payment processors that live inside your existing accounting or ERP software can handle all of this in the background. Platforms like EBizCharge, for example, build surcharging directly into their payment workflow and connect natively with major ERP and accounting systems. Surcharges are calculated, applied, and displayed automatically at the point of transaction. Your billing team doesn’t have to touch a thing.

Many of today’s payment platforms also use AI to handle the trickier parts of surcharge compliance, like monitoring state-by-state rule changes and flagging transactions that shouldn’t be surcharged. As AI continues to earn the trust of finance teams, these tools are only getting more reliable. The goal is to make surcharging invisible to your internal team while keeping it transparent to your customers.

Is Surcharging Right for Your Business?

Surcharging isn’t a universal fit. There are situations where it makes a lot of sense and others where it might not be the best move.

It tends to work well for B2B companies, professional services firms, distributors, and manufacturers. These are businesses where invoices are sizable and customers are other businesses that understand the economics of payment processing. It’s also a natural fit for companies with tight margins that can’t absorb processing fees without it affecting their bottom line.

On the other hand, if you’re a consumer-facing retailer in a highly competitive market, a surcharge might push customers toward a competitor who doesn’t charge one. All in all, your customer relationships matter most of all so understand how your customers might react when faced with a new surcharge fee.

Some payment platforms now use AI to analyze your transaction history and break down exactly how much you’re losing to processing fees by card type, customer, and payment channel. It’s part of a broader shift in how SMEs are using AI to manage financial operations. If the majority of your revenue comes through cards and your fees are eating into your margins, surcharging is worth a serious conversation with your finance team.

Where This Is All Headed

Credit card processing fees aren’t going away. If anything, they’re likely to keep climbing as card usage grows and interchange rates adjust. For years, businesses accepted these costs as just another line item on the P&L. That era is coming to an end.

Surcharging gives businesses a way to recover those costs without cutting into their margins or raising prices across the board. When it’s done right (transparently, compliantly, and with the right tools), it’s one of the simplest ways to put money back on the bottom line. The conversation around who pays for credit card processing is shifting. The only question is whether your business is going to be part of that shift, or watch it happen from the sidelines.

{kind=link}