A new analysis from San Francisco venture firm DVC contends that Wall Street and private markets are applying the wrong playbook to artificial intelligence companies — treating them like software businesses when they actually behave more like industrial operations.

The firm unveiled its State of AI Report, a living document that the partners say will evolve continuously rather than gather dust on a shelf. The report draws on more than a decade of AI investing, a synthesis of leading third-party research, and signals from a network of over 200 operators and investors.

DVC also announced The AI Rabbit Hole, an invitation-only gathering in San Francisco on June 5 where founders, researchers, and investors will debate the report’s themes.

The Inference Tax

The central argument cuts against a comfortable assumption in tech investing: that any company with “AI” in its pitch deck deserves a software-style valuation multiple.

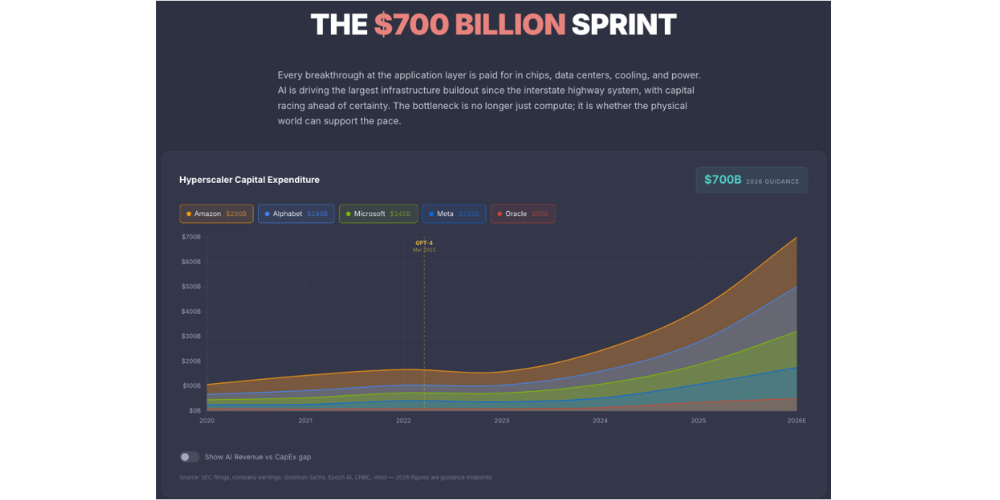

Classic SaaS economics rely on margins that can reach 80 percent at scale, the byproduct of code that costs almost nothing to replicate. AI startups don’t enjoy that luxury. Every query, every generated image, every agent action burns compute. DVC estimates that 40 to 60 percent of revenue at AI companies is swallowed by what the report calls an “inference tax” — the combined cost of GPUs, foundation model API calls, cloud capacity, and electricity.

The result, the report argues, is a margin profile that looks far more like manufacturing than like enterprise software.

Davidov reaches for an analogy from Nvidia chief executive Jensen Huang, who has described modern data centers as factories. “Your ‘AI agent for banking AML and compliance’ is not SaaS — it’s closer to a silverware customization service trying to build a brand,” Davidov said. “The spoons are mass-produced in a factory from sheet metal, sourced from mills that process ore from mines. Metal and electricity go in — consumer emotions, and some utility, come out.”

That framing doesn’t necessarily make today’s rich valuations wrong, he added — but it changes what investors are actually buying. “We’re not paying a premium for long-term terminal value, as with SaaS. We’re paying for much higher revenue growth potential.”

If margins on the model and infrastructure layers are headed toward commoditization, where does durable value sit? DVC’s answer points downstream: control of the user, ownership of the interface, distribution power, and the velocity of market capture. Upstream layers, in this view, increasingly resemble utilities.

A Different Growth Curve

The report also documents a scaling dynamic that has little precedent in software history. Small teams are crossing revenue thresholds in months that took the SaaS generation years. Perplexity AI, the report notes, reportedly added 50 percent to its annual recurring revenue in a single month to reach roughly $300 million. Higgsfield, an AI video startup, is cited as going from zero to $300 million in ARR within a year.

The full report is available at state-of-ai.dvc.ai.

{kind=link}